Originally published at Marketplace.

Inflation numbers came in better than expected this week, and they’re the latest in several months of data showing that price growth has slowed down. Another way to look at inflation came out from the Congressional Budget Office this week, looking at the issue from the lens of purchasing power. The CBO found that if you look at the same basket of goods from pre-pandemic to 2023, on average, Americans need less of their income to buy the same set of stuff. But if that just feels a bit off to you, I get it. According to the Congressional Budget Office, purchasing power went up across all income groups because incomes grew faster than prices between 2019 and 2023. “That kind of goes against the common perception of what’s going on is that people are losing purchasing power over the last few years,” said Vance Ginn who is president of Ginn Economic Consulting and was a White House chief economist during the Trump administration. The CBO found, percentage-wise, folks in the highest income bracket spent less of their income on common expenses — down 6.3%, thank you stock market. Folks in the lower income brackets weren’t so lucky. They saw only a two percent drop in how much they spent on basics, thanks to higher wages. But for people in the middle, it was even less noticeable. “And that’s why I think they’ve been, kind of, not being able to be as prosperous as some of the others during this period,” said Ginn. Plus these numbers reflect averages, not people’s individual experiences. And that’s where narratives really come into play, especially in an election year. “We did go through a period of about 18 months of very elevated inflation. But it’s also true that prices today are rising roughly in line with previous historical experience,” said Michael Linden, a Senior Policy Fellow at the Washington Center for Equitable Growth. And in campaign ads and in stump speeches we’ll probably end up hearing versions of both inflation stories, amplified in whichever direction benefits the candidate talking. “And I think that the American people are going to have to decide when they hear about inflation, which of those two things is more important to them,” said Linden. And whose narrative about the economy you choose to believe.

0 Comments

Originally published at Kansas Policy Institute.

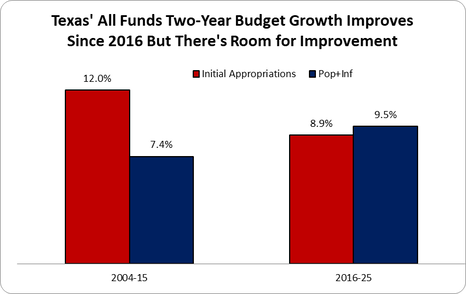

The death of HB 2663 in Kansas, which aimed to create new Sales Tax and Revenue (STAR) Bonds and Tax Increment Financing (TIF) districts for financing new sports stadiums, has reignited critical debate about the role of public funding in private projects. The bill also provided 100% financing for 30 years to attract the Kansas City Chiefs or Royals to new stadiums on the Kansas side of the KC Metro area. This follows after 58% of Jackson County voters wisely rejected a $2 billion subsidy for similar developments, highlighting a disconnection between rent seekers and the electorate’s preferences. These initiatives exemplify a deeper issue with economic development strategies that lean heavily on corporate welfare, undermining the principles of free-market capitalism that has long-supporting abundant prosperity. While Kansas ranks just 26th in its state business tax climate according to the Tax Foundation and 27th in economic outlook according to the American Legislative Exchange Council, picking winners and losers is the wrong approach. Stadium subsidies are intended to attract teams, showcasing the immediate allure of new facilities and jobs—the ‘seen’ effects. Yet, the ‘unseen’ consequences, including diverting substantial public funds from better uses and imposing long-term fiscal burdens on taxpayers, are far more concerning. Instead of acting as a neutral facilitator of economic activity, governments too often play favorites through these tax incentives, leading to market distortions and cronyism. The implications are significant: businesses spend more time lobbying for these financial boosts than focusing on consumer-driven growth and innovation. Milton Friedman famously criticized such government spending, stating, “There is nothing so permanent as a temporary government program.” In this context, the subsidies intended to be a short-term boost can lead to prolonged financial strain on public resources. Historically, STAR Bonds have fallen short of their promise to boost the commercial, entertainment, and tourism sectors. Despite using them for over two decades, these bonds have not elevated consumption in Kansas’s tourist-related sectors above the national average. Over a decade, tourist-related spending has notably declined, falling 20 percentage points below what might be expected compared to other states. This stark underperformance underscores the inefficacy of STAR Bonds in stimulating genuine economic growth. Moreover, the promise of job creation through such subsidies is often misleading. An analysis by the Kansas Policy Institute of Wichita’s Riverwalk and K-96/Greenwich STAR Bonds demonstrated that these projects did not spawn new employment but merely shifted jobs within the eastern side of Wichita, let alone the state. This job redistribution, rather than creation, suggests that such fiscal tools are not just ineffectual but harmful, as they concentrate development in ways that don’t align with the broader community interests. As manifested in STAR Bonds, corporate welfare fundamentally distorts the free market. It prompts businesses to seek profitability through government aid rather than market-driven innovation and efficiency. This misallocates precious resources and dampens the entrepreneurial spirit, crucial for real economic progress. Of course, many Kansans support the Royals or the Chiefs. These sports teams are part of the community and should be celebrated. And yet, they’re private businesses, and subsidizing their operations from the paychecks of someone in Edwardsville or Ellis County hardly seems appropriate. No matter how much you may cheer for Salvador Perez hitting a homer or Patrick Mahomes throwing another touchdown, these subsidies are no different than spending your paycheck to entire a battery factory in The Sunflower State. Milton Friedman argued that the government’s role should not be to determine economic winners and losers but to facilitate a stable environment that supports voluntary exchanges and organic growth. Therefore, policies should aim to reduce government expenditure, lower tax burdens, and ease regulations that impede business operations, fostering a climate where businesses can thrive on their merit. Moreover, funding these projects involves increased taxes or reallocating municipal funds, burdening local economies. The long-term financial commitments can lead to higher taxes elsewhere or cuts in essential services. Studies, such as those by the Brookings Institution, consistently show that stadium subsidies do not significantly increase local tax revenues or long-term employment growth. Instead, they often serve as handouts to billionaires at the expense of ordinary taxpayers. Despite its setbacks, the rejection of HB 2663 should be viewed as a protective measure against the continuation of flawed economic policies. It affirms commitment to market efficiencies over flashy, unproductive government expenditures. Policymakers must focus on long-term, sustainable strategies that benefit the wider population. With a special session looming, the idea of legislative-enacted, taxpayer-subsidized stadiums could still be alive in 2024. It’s troubling that while HB 2663 never got traction, the legislature actively removed oversight from some state incentive programs. Kansas must continue challenging economically unsound proposals and advocate for policies that lower business costs through reduced government spending, lower taxes, and less regulation. By promoting a more free-market environment, the state will ensure long-term economic health and prosperity for all Kansans, not just a select few. Government Spending Is The Problem The late, great economist Milton Friedman said, "The real problem is government spending." This is true as spending comes before taxes or regulations. In fact, if people didn't form a government or politicians didn’t create new programs, then there would be no need for government spending and no need for taxes. And if there was no government spending nor taxes to fund spending then there would be no one to create or enforce regulations. While this might sound like a utopian paradise, which I agree, there are essential limited roles for governments outlined in constitutions and laws. Of course, most governments are doing much more than providing limited roles that preserve life, liberty, and property. This is why I have long been working diligently for more than a decade to get a strong fiscal rule of a spending limit enacted by federal, state, and local governments promptly under my calling to "let people prosper," as effectively limiting government supports more liberty and therefore more opportunities to flourish. Fortunately, there have been multiple state think tanks that have championed this sound budgeting approach through what they've called either the Responsible, Conservative, or Sustainable State Budget. And recently I worked with Americans for Tax Reform to publish the Sustainable Budget Project, which provides spending comparisons and other valuable information for every state. Don't miss the latest updates as of April 2024. This groundbreaking approach was outlined recently in my co-authored op-ed with Grover Norquest of ATR in the Wall Street Journal. When Did This Budget Approach Begin? I started this approach in 2013 with my former colleagues at the Texas Public Policy Foundation with work on the Conservative Texas Budget. The approach is a fiscal rule based on an appropriations limit that covers as much of the budget as possible, ideally the entire budget, with a maximum amount based on the rate of population growth plus inflation and a supermajority (two-thirds) vote to exceed it. A version of this approach was started in Colorado in 1992 with their taxpayer's bill of rights (TABOR), which was championed by key folks like Dr. Barry Poulson and others. (picture below is from a road sign in Texas)  Why Population Growth Plus Inflation? While there are many measures to use for a spending growth limit, the rate of population growth plus inflation provides the best reasonable measure of the average taxpayer's ability to pay for government spending without excessively crowding out their productive activities. It is important to look at this from the taxpayer’s perspective rather than the appropriator’s view given taxpayers fund every dollar that appropriators redistribute from the private sector. Population growth plus inflation is also a stable metric reducing uncertainty for taxpayers (and appropriators) and essentially freezes inflation-adjusted per capita government spending over time. The research in this space is clear that the best fiscal rule is a spending limit using the rate of population growth plus inflation, not gross state product, personal income, or other growth rates. In fact, population growth plus inflation typically grows slower than these other rates so that more money stays in the productive private sector where it belongs. To get technical for a moment, personal income growth and gross state product growth are essentially population growth plus inflation plus productivity growth. There's no reasonable consideration that government is more productive over time, so that term would be zero leaving population growth plus inflation. And if you consider the productivity growth in the private sector, then more money should be in that sector at the margin for the greatest rate of return, leaving just population growth plus inflation. Population growth plus inflation becomes the best measure to use no matter how you look at it. Given the high inflation rate more recently, it is wise to use the average growth rate of population growth plus inflation over a number of years to smooth out the increased volatility (ATR's Sustainable Budget Project uses the average rate over the three years prior to a session year). And this rate of population growth plus inflation should be a ceiling and not a target as governments should be appropriating less than this limit. Ideally, governments should freeze or cut government spending at all levels of government to provide more room for tax relief, less regulation, and more money in taxpayers' pockets. Overview of Conservative Texas Budget Approach Figure 1 shows how the growth in Texas’ biennial budget was cut by one-fourth after the creation of the Conservative Texas Budget in 2014 that first influenced the 2015 Legislature when crafting the 2016-17 budget along with changes in the state’s governor (Gov. Greg Abbott), lieutenant governor (Lt. Gov. Dan Patrick), and some legislators. The 8.9% average growth rate of appropriations since then was below the 9.5% biennial average rate of population growth plus inflation since then, which this was drive substantially higher after the latest 2024-25 budget that is well above this key metric (before this biennial budget the growth rate was 5.2% compared with 9.4% in the rate of population growth plus inflation).  This approach was mostly put into state law in Texas in 2021 with Senate Bill 1336, as the state already has a spending limit in the constitution. The bill improved the limit to cover all general revenue ("consolidated general revenue") or 55% of the total budget rather than just 45% previously, base the growth limit on the rate of population growth times inflation instead of personal income growth, and raise the vote from a simple majority to three-fifths of both chambers to exceed it instead of a simple majority. There are improvements that should be made to this recent statutory spending limit change in Texas, such as adding it to the constitution and improving the growth rate to population growth plus inflation instead of population growth times inflation calculated by (1+pop)*(1+inf). But this limit is now one of the strongest in the nation as historically the gold standard for a spending limit of the Colorado's Taxpayer Bill of Rights (TABOR) has been watered down over the years by their courts and legislators, as it currently covers just 43% of the budget instead of the original 67%. My Work On The Federal Budget In The White House From June 2019 to May 2020, I took a hiatus from state policy work to serve Americans as the associate director for economic policy ("chief economist") at the White House's Office of Management and Budget. There I learned much about the federal budget, the appropriations process, and the economic assumptions which are used to provide the upcoming 10-year budget projections. In the President's FY 2021 budget, we found $4.6 trillion in fiscal savings and I was able to include the need for a fiscal rule which rarely happens (pic of President Trump's last budget).  Sustainable Budget Work With Other States and ATR When I returned to the Texas Public Policy Foundation in May 2020, as I wanted to get back to a place with some sense of freedom during the COVID-19 pandemic and to be closer to family, I started an effort to work on this sound budgeting approach with other state think tanks. This contributed to me working with many fantastic people who are trying to restrain government spending in their states and the federal levels. Here are the latest data on the federal and state budgets as part of ATR's Sustainable Budget Project. From 2014 to 2023, the following happened: Federal spending shot up by 81.7%, nearly four times faster than the 23.1% increase in the rate of population growth plus inflation.

Result: American taxpayers could have been spared more than $2.5 trillion in taxes and debt just in 2023 if federal and state governments had grown no faster than the rate of population growth plus inflation during the previous decade. And this would be even more if we considered the cumulative savings over the period.  My hope is that if we can get enough state think tanks to promote this budgeting approach, get this approach put into constitutions and statutes, and use it to limit local government spending as well, there will be plenty of momentum to provide sustainable, substantial tax relief and eventually impose a fiscal rule of a spending limit on the federal budget. This is an uphill battle but I believe it is necessary to preserve liberty and provide more opportunities to let people prosper. Sustainable State Budget Revolution Across The Country Below are the states (in alphabetical order) and state think tanks which I'm helping and information on how this process is going in those states. Here's an overview of this budgeting approach in Louisiana that can be applied elsewhere. I update these periodically, successful versus not successful budgeting attempts being 20-7 so far.

If you're interested in doing this in your state, please reach out to me. P.S. Good write-up on this issue here by Grover Norquist and I at WSJ, Dan Mitchell at International Liberty, and The Economist.  Originally published at The Center Square.

Iowa Gov. Kim Reynolds and the Republican-led Legislature have emphasized conservative budgeting as a central priority. Such prudence in budgeting is the cornerstone of fiscal conservatism, and the recent passage of the FY 2025 budget in Iowa highlights a commitment to fiscal restraint, albeit less stringent than in previous sessions. The newly approved $8.9 billion FY 2025 General Fund budget marks a 4.7 percent increase from the previous fiscal year's $8.5 billion, demonstrating moderate fiscal growth. Historically, spending has been recommended to align with the combined rates of population growth and inflation. Based on this formula, the FY 2024 budget of $8.5 billion should ideally have capped the FY 2025 spending at $8.8 billion. Adhering to such metrics ensures that the budget reflects the average taxpayer's ability to fund it, a fundamental principle that should guide all budgetary decisions. This year, however, the legislature has ventured slightly beyond this benchmark, underscoring the careful balance between fiscal responsibility and the needs of a growing state. To provide substantial relief to individual taxpayers, the legislature has implemented a significant income tax cut, which accelerates the implementation of a 3.8 percent flat tax in 2025. This measure is projected to save taxpayers over $1 billion. The tax relief directly benefits Iowans, putting more money back into their pockets and supporting more economic growth. Despite concerns from critics who argue that such fiscal strategies could undermine public services, the FY 2025 budget demonstrates that the government is not retrenching but rather growing at a deliberate pace. Education remains a top priority, accounting for 56 percent of the budget. When combined with the allocations to the Department of Human Health Services (DHHS), these two areas consume a significant 81 percent of the General Fund. While this concentration of funds reflects the importance placed on these sectors, it also highlights the challenges of allocating resources to other critical areas, such as public safety and the judicial system, which have only seen modest increases. The practice of conservative budgeting is further evidenced by the state's adherence to its legal spending cap, which allows up to 99 percent of projected revenue to be used. In contrast, the FY 2025 budget only commits 92 percent of these projections, reinforcing Iowa's fiscal discipline. This cautious approach is proving effective, as evidenced by the substantial budget surpluses recorded in recent years, including a $1.8 billion surplus in FY 2023, with similar surpluses anticipated for FY 2024 and FY 2025. Looking ahead, legislators must remain vigilant to ensure that conservative budgeting principles continue to guide fiscal policy. State Sen. Jason Schultz rightly points out the interdependence of tax policy and spending, “Both Republicans and Democrats need to realize that tax policy is affected by spending. And when you start seeing spending creeping up for annual, year after year, new good ideas, you can’t have good tax policy.” Strengthening Iowa's 99 percent spending limitation would provide a robust mechanism to curb future expenditure desires. This could be done by changing the law and enshrining it in the Constitution to bind spending increases to no more than the rate of population growth plus inflation. Iowa’s fiscal approach starkly contrasts the situations unfolding in neighboring states like Minnesota and Illinois or others such as New York and California. Higher spending and taxes in these progressive states contribute to economic challenges and drive more people away. The message is clear: unsustainable increases in spending can lead to severe consequences. Iowa's success in maintaining fiscal discipline through conservative budgeting and responsible tax policies is a testament to the effectiveness of this approach. Iowa’s unwavering commitment to conservative budgeting and responsible tax policies is the cornerstone of its fiscal strategy, ensuring the state remains a model of stability and prosperity. By striking a balance between providing essential services and fostering economic growth, Iowa sets a commendable example of how sustainable fiscal policies can safeguard a state’s financial health and support the well-being of its citizens. Dive into this week's hot economic topics in just 12 minutes on "This Week's Economy"! 🕒

I tackle big questions: 🌍 Are humans driving climate change? 📊 What's the latest in the U.S. labor market? 🌟 How are Texas and Louisiana setting examples of prosperity? Don’t just listen—engage! Share your thoughts, rate me, and leave a review. For in-depth insights and show notes, subscribe to my Substack at vanceginn.substack.com or visit vanceginn.com. #economy #SocialSecurity #Medicare #ClimateChange  Originally published at The Courier.

By John Hendrickson and Vance Ginn, Ph.D. Iowa Governor Kim Reynolds and the Republican-led Legislature have emphasized conservative budgeting as a central priority. Such prudence in budgeting is the cornerstone of fiscal conservatism, and the recent passage of the FY 2025 budget in Iowa showcases a commitment to fiscal restraint, albeit less stringent than in previous sessions. The newly approved $8.9 billion FY 2025 General Fund budget marks a 4.7 percent increase from the previous fiscal year's $8.5 billion, demonstrating moderate fiscal growth. Historically, spending has been recommended to align with the combined rates of population growth and inflation. Based on this formula, the FY 2024 budget of $8.5 billion should ideally have capped the FY 2025 spending at $8.8 billion. Adhering to such metrics ensures that the budget reflects the average taxpayer's ability to fund it, a fundamental principle that should guide all budgetary decisions. This year, however, the legislature has ventured slightly beyond this benchmark, underscoring the careful balance between fiscal responsibility and the needs of a growing state. To provide substantial relief to individual taxpayers, the legislature has implemented a significant income tax cut, reducing the flat tax rate to 3.8 percent. This measure is projected to save each taxpayer over $1 billion annually. The tax relief directly benefits Iowans, putting more money back into their pockets and supporting more economic growth. Despite concerns from critics who argue that such fiscal strategies could undermine public services, the FY 2025 budget demonstrates that the government is not retrenching but rather growing at a deliberate pace. Education remains a top priority, accounting for 56 percent of the budget. When combined with the allocations to the Department of Human Health Services (DHHS), these two areas consume a significant 81 percent of the General Fund. While this concentration of funds reflects the importance placed on these sectors, it also highlights the challenges of allocating resources to other critical areas, such as public safety and the judicial system, which have only seen modest increases. The practice of conservative budgeting is further evidenced by the state's adherence to its legal spending cap, which allows up to 99 percent of projected revenue to be used. In contrast, the FY 2025 budget only commits 92 percent of these projections, reinforcing Iowa's fiscal discipline. This cautious approach is proving effective, as evidenced by the substantial budget surpluses recorded in recent years, including a $1.8 billion surplus in FY 2023, with similar surpluses anticipated for FY 2024 and FY 2025. Looking ahead, legislators must remain vigilant to ensure that conservative budgeting principles continue to guide fiscal policy. State Senator Jason Schultz rightly points out the interdependence of tax policy and spending, “Both Republicans and Democrats need to realize that tax policy is affected by spending. And when you start seeing spending creeping up for annual, year after year, new good ideas, you can’t have good tax policy.” Strengthening Iowa's 99 percent spending limitation would provide a robust mechanism to curb future expenditure desires. This could be done by changing the law and enshrining it in the Constitution to bind spending increases to no more than the rate of population growth plus inflation. Iowa’s fiscal approach starkly contrasts the situations unfolding in neighboring states like Minnesota and Illinois or others such as New York and California. Higher spending and taxes in these progressive states contribute to economic challenges and drive more people away. The message is clear: unsustainable increases in spending can lead to severe consequences. Iowa's success in maintaining fiscal discipline through conservative budgeting and responsible tax policies is a testament to the effectiveness of this approach. Iowa’s unwavering commitment to conservative budgeting and responsible tax policies is the cornerstone of its fiscal strategy, ensuring the state remains a model of stability and prosperity. By striking a balance between providing essential services and fostering economic growth, Iowa sets a commendable example of how sustainable fiscal policies can safeguard a state’s financial health and support the well-being of its citizens. John Hendrickson serves as policy director of Iowans for Tax Relief Foundation, and Vance Ginn, Ph.D., is a contributing scholar at ITR Foundation and former chief economist at the Office of Management and Budget, 2019-20. Originally published at Texans for Fiscal Responsibility.  Executive Summary

Could Colorado become one of the seven states with no income tax? Vance Ginn, former White House Office of Management and Budget, believes the state is on the #Path2Zero.

Originally published at Washington Times.

In President Biden‘s recent State of the Union address, he painted a rosy economic picture, touting what he called “Bidenomics” as the driving force behind what he claims is a robust economy. He pointed to a low unemployment rate, the absence of a recession, and a lower inflation rate as evidence of success. Reality, however, tells a different story. And Mr. Biden’s recently released irresponsible budget sends the federal government and America further toward bankruptcy. Despite the president’s assertions, the economy and inflation remain top concerns for most Americans. The disconnect between the headlines and the lives of ordinary citizens underscores the profound challenges facing the nation’s economic landscape. This sense of malaise can be directly attributed to the flawed principles underlying Bidenomics, as outlined in his latest budget. These include excessive spending, taxation and regulation. Each is destructive, but together, they are catastrophic. The result has been stagflation and less household employment in four of the last five months. There have also been lower inflation-adjusted average weekly earnings by 4.2% since January 2021, when Mr. Biden took office. Rather than fostering economic growth and prosperity, Bidenomics has stifled innovation, investment and job creation. At its core, Bidenomics represents a misguided attempt to address complex economic issues through heavy-handed government intervention. While the administration may tout short-term gains, the long-term consequences of such policies are far-reaching and unaffordable. The reality is that excessive government spending has led to unsustainable levels of debt, burdening future generations with the consequences of fiscal irresponsibility. Similarly, excessive taxation is stifling entrepreneurship and dampening economic activity, limiting opportunities for individuals and businesses alike. Excessive regulation serves only to hamper innovation and drive up costs, exacerbating the challenges facing working families. Unfortunately, Mr. Biden’s latest budget proposal doubles down on these bad policies. Even with rosy assumptions of tax collections being a higher share of economic output over time as the tax hikes will reduce growth and, therefore, lower taxes as a share of gross domestic product, the budget continues massive deficits every year. This will result in higher interest rates, higher inflation, more investment These results have been highlighted in economic theory by economists such as Alberto Alesina and John B. Taylor. Their research has found that raising taxes doesn’t help close budget deficits because of the reduction in growth from higher taxes in a dynamic economy. The way forward should be cutting or at least better-limiting government spending — the ultimate burden of government on taxpayers. Amid these challenges, America also needs a return to optimism and flourishing. This includes leadership that inspires confidence, fosters innovation, and empowers people to pursue their dreams. We need out-of-the-box policies prioritizing economic freedom and individual opportunity, allowing the entrepreneurial spirit to thrive and driving growth and prosperity. More specifically, this means reducing the burden of government intervention through lower spending and taxes, streamlining regulations, and fostering an environment where entrepreneurship can thrive. By embracing fiscal sustainability and making tough choices, we can ensure the long-term stability and prosperity of our nation. In short, while Mr. Biden tries to spin a positive narrative about the economy, the facts speak for themselves. We cannot afford Bidenomics, no matter the headlines, what was touted in the State of the Union address, or the latest budget. The stakes are too high, and the consequences too grave, to ignore the reality of our economic situation. We need leadership that is willing to confront the hard truths and enact policies that prioritize the well-being of all Americans, fostering an environment where optimism and flourishing can thrive.  Originally published at Law & Liberty.

The Congressional Budget Office (CBO) just released the February 2024 Budget and Economic Outlook, and projections look grim. This year, net interest cost—the federal government’s interest payments on debt held by the public minus interest income—stands at a staggering $659 billion in 2023 and has recently soared to about $1 trillion. Unless politicians face these facts and restrain spending, Americans can expect rising inflation and painful tax hikes without improvement in public services. Some politicians quickly blamed a lack of tax revenue, calling for repealing the 2017 Trump tax cuts. But how much more money can they take? New IRS data shows that 98% of all income taxes are paid by the top 50% of income earners, those making at least $46,637. Moreover, 35% of Americans feel worse off than 12 months ago and inflation remains the primary concern for those across the income spectrum. So perhaps, rather than taking more money, the government should own up to its mistakes. The massive net interest costs result from bad spending habits, not a lack of revenue. This requires the federal government to adopt strict fiscal and monetary rules to rein in wasteful deficit spending and money printing that fuel higher interest rates and inflation. Net interest cost is the second largest taxpayer expenditure after Social Security and is higher than spending on Medicaid, federal programs for children, income security programs, or veterans’ programs. And it’s expected to grow. The CBO projects net interest to surpass Medicare spending this year and balloon to $1.6 trillion in 2034 as a result of higher debt and higher interest rates. Interest rates on Treasury debt are at the highest since 2007, paying between 4% and 5.5%, and the rates are expected to rise further. As the stockpile of gross federal debt is expected to grow by about $20 trillion to $54 trillion over the next decade, politicians will face an increasing temptation to rely on the Federal Reserve to pay for it by printing money. If the Fed does, the dollar’s value will decline, and Americans will continue to struggle financially. In an ideal world, politicians will organize the budget process to focus on funding a limited government and ensuring Americans keep their hard-earned money. They would also have plans to cut spending during times of economic downturn to reduce tax burdens on families and businesses and avoid the Keynesian fallacies of deficit spending to fill gaps in economic growth. However, America isn’t Shangri-La. As Thomas Sowell poignantly notes, a politician’s first goal is to get elected, the second goal is to get reelected, and the third goal is far behind the first two. So long as there are investors happy to purchase Treasury debt, there will be politicians who are happy to sway voters with generous spending programs financed by public debt. This must end. Instead, Washington should require strong institutional constraints with a spending limit. The limit should cover the entire budget and hold any budget growth to a maximum rate of population growth plus inflation. This growth limit represents the average taxpayer’s ability to pay for spending. Following this limit from 2004 to 2023 would have resulted in a $700 billion debt increase instead of the actual increase of $20 trillion. Such a policy has been in effect in Colorado since 1992. It is the Taxpayer’s Bill of Rights (TABOR) amendment to the Colorado Constitution. TABOR has revenue and expenditure limitations that apply to state and local governments. The revenue limitation applies to all tax revenue, prevents new taxes and fees, and must be overridden by popular vote. Expenditures are limited to revenue from the previous year plus the rate of population growth plus inflation. Any revenue above this limitation must be refunded with interest to Colorado citizens. A spending cap like TABOR is necessary but not sufficient to solve the problem because politicians in Washington can still pressure the Federal Reserve to pay for the increased debt by printing money. Therefore, it must be combined with a monetary rule to force fiscal sustainability while requiring sound money with fewer distortions in the economy. Monetary rules can come in many forms. While no rule is perfect, research shows that a rule-based monetary policy can result in greater stability and predictability in money growth than the current policy of “Constrained Discretion” whereby the Fed follows rules during “normal times” and has discretion during “extraordinary times.” Whether we are in ordinary or extraordinary times is up to policymakers, who typically don’t want to “let a good crisis go to waste,” as they say. Milton Friedman advocated for a money growth rate rule, the “k-percent rule.” This rule states that the central bank should print money at a constant rate (k-percent) every year. A variation of this rule was used by Fed Chair Paul Volcker in the late 1970s and early 1980s to tackle the Great Inflation with much success. Unfortunately, the Fed had already done too much damage with excessive money growth before then, so the cuts to the Fed’s balance sheet contributed to soaring interest rates that forced destructive corrections in the economy, resulting in a double-dip recession in the early 1980s. This led to the Fed abandoning money growth targeting in October 1982. It is important to note, though, that this “monetarist experiment” was not bound to any law, constitutional or statutory. During that time, the Fed still operated under discretion, which is why it was able to abandon the monetary growth rule just a few years after it had begun, unfortunately. There are other rules that could be applied. John Taylor proposed what’s been coined the Taylor Rule, which estimates what the federal funds rate target, which is the lending rate between banks, should be based on the natural rate of interest, economic output from its potential, and inflation from target inflation. Scott Sumner most recently popularized nominal GDP targeting, which uses the equation of exchange to allow the money supply times the velocity of money to equal nominal GDP. It has different variations, but the key is that velocity changes over time, so the money supply should change based on money demand to achieve a nominal GDP level or growth rate over time. By focusing on a rules-based approach to spending and monetary policy, Americans do not have to worry about electing the perfect candidate every election. Proper constraints will nudge even the worst politicians to make fiscally responsible choices and reduce net interest costs. Furthermore, America will be better positioned to respond to crises at home and abroad. If Congress wants to see who is to blame for the grim CBO projections, they should look in the mirror. Stop looking to take hard-earned money away from Americans and focus on sound budget and monetary reforms now.  Originally published at The City Journal.

In November 2023, Texas voters approved a constitutional amendment, HJR 2, which Governor Greg Abbott said would “ensure more than $18 billion in property tax cuts—the largest property tax cut in Texas history.” Texas homeowners’ hopes were dashed at the start of 2024, however, when they got their property tax bills. The promised $18 billion reduction amounted to only $12.7 billion in new property tax relief, a fraction of the state’s record $32.7 billion budget surplus, while the other $5.3 billion merely maintained property tax relief from years past. While Texas doesn’t have a state income tax, it does have the nation’s sixth-most burdensome property taxes. These taxes obstruct peoples’ ability to buy homes and price others out of the homes they’re in. Texans expect and deserve clarity about their property tax bills, but state policymakers’ failed promises and lack of transparency have eroded public trust. Despite the governor’s claim, the 2023 tax relief package, spread over two years, isn’t even the state’s largest historic property tax cut. In 2006, the Texas legislature apportioned $14.2 billion to reducing residents’ property taxes, cutting school district maintenance and operations (M&O) property tax rates by a third for 2008–09 biennium, and making up the difference with a revised franchise tax, a higher cigarette tax, and a higher motor vehicle sales tax. Adjusted for inflation, 2023’s cut would have had to exceed $21 billion to surpass the 2006 cut. The new package's biggest achievement was saving taxpayers $5 billion in 2023 by reducing the maximum school district M&O property tax rate by 10.7 cents per $100 valuation; it also raised the homestead exemption of taxable value for school district M&O property taxes to $100,000 and limited appraisal-value increases to 20 percent for other property. And yet, Texans’ total property taxes paid in 2023 nevertheless rose by $165.2 million over 2022, an overall increase of 0.4 percent. That net increase came from school district tax hikes to fund more debt ($890.2 million); municipal governments ($1.3 billion); county governments ($1.5 billion); and special purpose districts ($1.5 billion). These hikes effectively washed away state-level reductions. While this result is ultimately the fault of local governments, the state should have done more to provide relief and restrict localities’ spending and taxes. This growth in local property tax collections is part of a larger trend. From 1998 to 2023, Texas’s total property taxes collected rose 338 percent while the rate of population growth plus inflation was just 136 percent. No wonder so many Texans feel as though they are being crushed by housing unaffordability. How can Texas fix its spending problem? Rather than resort to temporary fixes, the state needs a robust spending cap in its constitution like Colorado’s Taxpayer’s Bill of Rights (TABOR), which limits state and local government spending increases to no more than the rate of population growth plus inflation. Though Colorado’s TABOR has been the gold standard for a state spending limit since its enactment in 1992, it can be improved. At this time, TABOR applies to Colorado’s general revenue, less than half of its total funds; it should be expanded to apply to all state funds, which would account for about two-thirds of its budget, as originally intended. Texas, or Colorado itself, could also improve the model by replacing the latter’s policy of refunding excess tax revenue to taxpayers with up-front income-tax-rate cuts. Texas enacted a statutory spending limit in 2021, but it lacks teeth, as an overriding constitutional spending limit covers just 45 percent of the budget and can be exceeded by a simple majority. In conjunction with a stronger constitutional spending limit, the Texas legislature should implement strategic budget cuts. These efforts combined with the stricter constitutional spending limit would create opportunities for surpluses at the state and local levels, which would pave the way for the state to reduce school M&O property taxes annually until they are fully eliminated. This alone would shave off nearly half of the property tax burden in Texas. Viewed from the coasts, Texas is a beacon of economic freedom. But as its spending and property tax data show, it isn’t perfect. The Texas legislature should acknowledge its failed promises and deliver real property tax relief for its citizens.  Originally published at Dallas Express.

Home “owners” in Dallas and surrounding cities find themselves grappling with the weight of unaffordability as property taxes soar, increasing by $120 million despite the touted cuts at the end of 2023. A recent study reveals the burden on renters in Texas and nationwide, with many paying over 30% of their monthly income on housing. A factor contributing to this rising cost of renting, and housing in general, is soaring property taxes. The predicament stems from excessive state and local spending and purported property tax “cuts” that too often merely shift the burden through exemptions. Renters, technically anyone with a monthly payment or a mortgage since homeowners are just renting from the government, bear the brunt of this financial strain, emphasizing the urgent need for fiscal reform. Late last year, Dallas residents witnessed a modest one-cent property tax reduction rate, with surrounding cities experiencing varying degrees of reduction. Fort Worth saw a 4-cent reduction, and McKinney a 3-cent reduction. Despite these adjustments, most cities, including Dallas, faced increased property taxes eclipsed by rising spending and housing appraisals. Even in Plano, recognized for its low property taxes in the DFW area, homeowners will endure higher monthly property tax amounts due to home valuation hikes. The incongruity between property tax decreases and housing cost increases is alarming, prompting a closer look at the numbers. According to Axios, the average taxable value of homes in Denton County rose from approximately $402,000 in 2022 to around $449,000 in 2023. Similarly, the average market value of Collin County homes increased from about $513,000 in 2022 to roughly $584,000 in 2023. One doesn’t need to be a mathematician to recognize how a property tax decrease of even a few cents doesn’t begin to keep pace with skyrocketing home valuations and rent. No wonder 20% of Dallas homebuyers looked to get out of the city last year. The crux of the issue lies in reining in local spending. The axiom holds: the burden of government is not how much it taxes but how much it spends. Dallas, with its escalating budget that reached a historic high last year, renders proposed property tax cuts inconsequential. My new research released by Texans for Fiscal Responsibility highlights how property taxes continued to go up last year by $165 million, even with the Texas Legislature passing $12.7 billion in new property tax relief. This ended up being the second largest property tax relief in Texas history, not the largest as many politicians have been claiming since last July, which is what I wrote then. The best path for Texans is to finally have their right to own their prosperity instead of renting from the government by paying property taxes forever. This can be done by restraining state and local government spending and using resulting state surpluses to reduce school property tax rates until they’re zero. And by local governments, including Dallas, using their resulting surpluses to reduce their property tax rates until they’re zero. Dallas must adopt a spending limit, one that does not permit the budget to exceed the rate of population growth rate plus inflation – a measure aligned with what the average taxpayer can afford. Performance-based budgeting and independent efficiency audits, preferably conducted by private auditors, should identify opportunities for improvements and reductions in ineffective programs, helping provide more opportunities for property tax relief. Dallas leaders can empower their constituents by redirecting taxpayer money to them while funding limited government. The adoption of these strategic measures not only benefits homeowners but extends its positive impact to renters and business owners, providing tangible rewards for their hard work and fostering a more economically vibrant community. Dallas leaders are responsible for ushering in a new era of fiscal responsibility that ensures affordability for all residents and supports sustained economic growth. The path to long-lasting property tax relief is clear: let’s seize this opportunity for positive change and secure a brighter, more prosperous future for Dallas.  Originally published at American Institute for Economic Research.

Recent headlines for the January jobs report indicate a robust economy. But a more thorough look reveals challenges for Americans. One recent headline proclaimed “Voters are finally noticing that Bidenomics is working.” But just 30 percent of Americans think the economy is doing well. When asked who would handle the economy better, people give former president Donald Trump a 22-point advantage over President Biden. Challenges include increasing part-time employment in recent months, declining household employment in three of the last four months for a net decline of 398,000 job holders, mounting public debt burdens, and declining real wages, which have fallen by 4.4 percent since January 2021. Why these results? Bidenomics is based on costly Keynesian boom-and-bust policies. With so much whiplash, it’s no wonder people are conflicted about the economy. In the latest jobs report for January, a net increase of 353,000 nonfarm jobs from the establishment survey appears robust, as it was well above the consensus estimate of 185,000 new jobs. But let’s dig deeper. Last month, household employment declined by 31,000, contradicting the headlines. The divergence of jobs added between the household survey and the establishment survey has widened since March 2022. This period coincides with declining real gross domestic product in the first and second quarters of 2022 (usually that’s deemed a recession, but it hasn’t been yet). Indexing these two employment levels to 100 in January 2021, they were essentially the same until March 2022, but nonfarm employment was 2.5 percent higher in January 2024. While this divergence mystifies some, a primary reason is how the surveys are conducted. The establishment survey reports the answers from businesses and the household survey from individual citizens. The establishment survey often counts the same person working in multiple jobs, while the household survey counts each person employed. This likely explains much of the divergence, as many people work multiple jobs to make ends meet. The surge in part-time employment and more discouraged workers underscores the fragility of the labor market. Though average weekly earnings increased by 3 percent in January over a year prior, this is below inflation of 3.1 percent. Real average weekly earnings had increased for seven months before falling last month. And there had been declines in year-over-year average weekly earnings for 24 of the prior 25 months before June 2023. These real wages are down 4.4 percent since Biden took office in January 2021. As purchasing power declines, mounting debts become more urgent. Total US household debt has reached unprecedented levels, with credit card debt soaring by 14.5 percent over the last year to a staggering $1.13 trillion in the fourth quarter of 2023. Such substantial growth in debt raises concerns about the current (unsustainable?) consumption trends, business investment, and a looming financial crisis. The surge in mortgage rates to over seven percent for the first time since December and rising home prices exacerbate housing affordability challenges, particularly for aspiring homeowners. An integral component of what some consider the “American Dream,” housing affordability is a major factor discouraging Americans. The euphoria surrounding the January 2024 jobs report is misplaced. Policymakers should heed these warning signs and enact meaningful reforms to address root causes. Biden’s policy approach undergirds most of these difficulties. Bidenomics focuses on his Build Back Better agenda that picks winners and losers by redistributing taxpayer money for supposed economic gains through large deficit spending. We haven’t seen an agenda of this magnitude since LBJ’s Great Society in the 1960s or possibly since FDR’s New Deal in the 1930s. Both were damaging, as the Great Society dramatically expanded the size and scope of government, contributing to the Great Inflation in the 1970s, and the New Deal contributed to a longer and harsher Great Depression. Just since January 2021, Congress passed the following major spending bills upon request of the Biden administration:

These four bills will add nearly $4.3 trillion to the national debt. But at least another $2.5 trillion will be added to the national debt for student loan forgiveness schemes, SNAP expansions, net interest increases, Ukraine funding, PACT Act, and more. In total over the past three years, excessive spending will lead to more than $7 trillion added to the national debt, which now totals $34 trillion — a 21 percent increase since 2021. There seems to be no end to soaring debt with the recent discussions of more taxpayer money to Ukraine, Israel, the border, and the “bipartisan tax deal,” collectively adding at least another $700 billion to the debt over a decade. Record debts accrued by households and by the federal government (paid by households) are not signs of a robust economy. This will likely worsen before it improves, as household savings dry up. And with interest rates likely to stay higher for longer because of persistent inflation, debts will crowd out household finances and the federal budget. The Federal Reserve has monetized much of this increased national debt over the last few years by ballooning its balance sheet from $4 trillion to $9 trillion and back down to a still-bloated $7.6 trillion. This helps explain persistent inflation, massive misallocation of resources, and costly malinvestments across the economy, keeping the economy afloat yet fragile. Excessive deficit spending weighs heavily on future generations, saddling them with unsustainable debt levels they have no voice in. Today, everyone owes about $100,000, and taxpayers owe $165,000, toward the national debt. Of course, these amounts don’t include the hundreds of trillions of dollars in unfunded liabilities for the quickly-going-bankrupt welfare programs of Social Security and Medicare. Future generations will be on the hook for even more national debt if Bidenomics continues and Congress doesn’t reduce government spending now. This is why the national debt is the biggest national crisis for America. We’re robbing current and future generations of their hopes and dreams. Fortunately, there’s a better path forward if politicians have the willpower. This path should be chosen before we reap the major costs of a bigger crisis. I’ve recently outlined what this should look like at AIER. In short, we need a fiscal rule of a spending limit covering the entire budget based on a maximum rate of population growth plus inflation. There should also be a monetary rule that ideally reduces and caps the Fed’s current balance sheet to at least where it was before the lockdowns. My work with Americans for Tax Reform shows that had the federal government used this spending limit over the last 20 years, the debt would have increased by just $700 billion instead of the actual $20.2 trillion. That’s much more manageable and would point us in a more sustainable fiscal and monetary direction. Together, fiscal and monetary rules that rein in government will help reduce the roles that politicians and bureaucrats have in our lives so we can achieve our unique American dreams. If not, we will have wasted many dreams on Bidenomics that can make things look good on the surface, but cause rot underneath. Healthcare Costs Are Straining Federal And Household Budgets. Here’s How Biden Can Rein Them In2/14/2024  Originally published at Daily Caller.

Soaring health care spending continues to spiral up, tightening the financial noose on households and government coffers. Families are forced to make difficult choices between paying for essential medical care and meeting basic needs while the federal government struggles to rein in spending amid mounting debt. These soaring health care costs must be addressed with market-based approaches before it’s too late. When the Affordable Care Act (ACA) was passed in 2010, it was heralded as the panacea for reining in healthcare costs. However, the law’s complex regulations and mandates have contributed to administrative bloat and increased overhead costs, ultimately driving up premiums and out-of-pocket patient expenses. Unfortunately, since then, subsequent politicians have failed to correct course. In 2024, federal spending on Medicare, Medicaid, and ACA subsidies will likely exceed the discretionary budget, posing a significant threat to long-term fiscal sustainability. Compulsory spending on health coverage in the private sector infringes upon household earnings. This exacerbates economic challenges for families whose purchasing power is already reduced, as inflation-adjusted average weekly earnings are down 3.1 percent since Jan. 2021. Moreover, the growing burden of health care spending poses a significant threat to long-term fiscal sustainability, as rising debt levels raise concerns about future economic prosperity. The Congressional Budget Office (CBO) recently released its annual Budget and Economic Update, painting a grim budget picture. The trajectory is alarming, with expenditures expected to be $6.4 trillion this fiscal year before soaring to a staggering $10.1 trillion by 2034. Also, net interest spending is poised to balloon from $1 trillion to $1.6 trillion by 2034. These projections underscore the urgent need for meaningful reforms to rein in healthcare costs and put the federal budget on a more sustainable path. To address these challenges, policymakers must prioritize fiscal responsibility and adopt measures to remove government as much as possible from healthcare. This would help to quickly get healthcare back to a relationship between a doctor and patient. Today, too many middle layers rob time between the doctor and patient and raise healthcare prices. Policymakers should make market-based reforms. It won’t be done overnight, so there will need to be some steps to get there. It would be great if just making healthcare prices transparent would solve the problem. But the healthcare system is much more dysfunctional than that, unfortunately. Many reimbursement rates are set between doctors and private insurance companies or government programs like Medicaid and Medicare. Those reimbursement rates are so different depending on which entity is negotiating that the prices won’t tell us much, other than how screwed up the system is, but we already know that. A market-based approach should remove obstacles on the demand and supply sides of the market. This should include ending the tax exclusion for employer-sponsored health insurance. There’s a long history of this exclusion, which started during WWII. But while it had good intentions, the result has been a major distortion to the healthcare market. There should also be consideration of a voucher program for Medicare and block grants to states for Medicaid with limited growth each year. These would help reduce the moral hazard and over-subsidization on the demand side. On the supply side, the federal and state governments should remove rules that restrict the supply of doctor offices by removing certificate of need laws. They can also boost the supply of physicians by reducing or eliminating occupational licenses. Unleashing supply and imposing market forces on demand will result in more innovative, affordable, and accessible care for everyone. The resulting reduction in government spending and improved timely access to quality care can help support more prosperity. This would reduce the need for people on government safety net programs. It would also help mitigate higher prices, alleviate strain on household budget burdens, and safeguard the nation’s economic future. These steps will require difficult choices and bipartisan cooperation at the federal and state levels, but the stakes are too high to ignore the issue any longer.  Originally published at Kansas Policy Institute. Kansas, like most states, has a spending problem, not a revenue problem. The 2025 Responsible Kansas Budget offers several ways that the state can limit its spending to pave the way for tax reform and economic growth in the future. In June 2023, Kansas ended FY 2023 with collected tax revenues at $10.2 billion – a 4.1% or $402 million increase over the collected tax revenues of FY 2022. According to the Kansas Legislative Research Department, even if Kansas had enacted a flat tax bill during its 2023 legislative session, the state would end FY 2028 with $2.7 billion in its ending balance and $1.8 billion in the Budget Stabilization Fund, totaling $4.5 billion in reserves. At the same time, spending has grown massively over the last decade. According to the FY 2025 Governor’s Budget Report, the approved FY 2024 General Fund budget of $9.918 billion is 13.6% more than the approved 2023 budget. In FY 2020, the State Fund appropriations equaled $12.6 billion, but has ballooned into and after the COVID-19 pandemic to be $19 billion in FY 2023 and a base of $18.4 billion for FY 2024. If Kansas’s annual appropriations had grown at the rate of population growth plus inflation since FY 2005, State Fund appropriations would be $6.4 billion lower in FY 2024 than the actual base appropriations. This equates to a $46.6 billion cumulative difference from FY 2005 to FY 2024. What this number represents is higher taxes on Kansans, slower economic growth, and fewer opportunities for people to flourish.  Originally published at Pelican Institute.

Spending, not taxes, is the ultimate burden of government. If you don’t spend money on a program, you don’t need to collect taxes to fund it. And if you don’t spend money on programs, the government can’t regulate things. Remember that government spending is paid for by the people, as the government creates nothing to earn income, so considering what people can afford is crucial. This is why it’s essential for governments at every level to narrow their scope to the essential functions enshrined in constitutions. Otherwise, spending grows too much and results in taxes being too burdensome on people. Governments across the country and the globe are spending too much. And it appears that a sustainable budget revolution is happening! I’ve been working for over a decade to help state, federal, and local governments create and adopt sustainable budgets that fund limited government. This is critical to keeping taxes and regulations lower than otherwise, so families and entrepreneurs have more of their hard-earned money in their pockets. This standard is called a fiscal rule or a tax and expenditure limit (TEL), which goes like this: a government’s budget growth cannot exceed the rate of population growth plus inflation. How does this simple rule work? This approach started in 2013 when I helped develop the Conservative Texas Budget. After years of excessive spending in Texas, we defined the narrative of a tangible cap on appropriations based on the rate of population growth plus inflation. There was no change in the state’s law right away, but this approach worked well for several sessions by helping keep spending within this rate, which represents the average taxpayer’s ability to pay for spending. Importantly, this is a maximum growth limit, as most states need to spend much less than this limit as they are already spending too much, which will help leave more money in people’s pockets. Over the years, this rule has been used to help state and local governments make their budgets more sustainable. One such victory came in 2021 when Texas put Senate Bill 1336 into law. The bill changed the state’s budget limit to not exceed the rate of population growth and inflation when it had been based on personal income growth. This was an extraordinary reform that took nearly a decade to accomplish. It’s not perfect, as it should be in the state’s constitution and should cover all state funds and use population growth plus inflation. But it’s one of, if not the, best in the country. The other spending limit that has long been the gold standard is the Taxpayer’s Bill of Rights (TABOR) in Colorado, which I recently outlined how it needed to be improved as it has been weakened over time. By working with think tanks, grassroots organizations, and lawmakers across the country, I’ve helped create and pass sustainable budgets for the following states: Alaska, Florida, Iowa, Michigan, Mississippi, Montana, South Carolina, and Tennessee. I’ve also worked with other states where a sustainable budget was proposed, such as Kansas and Louisiana, but hasn’t yet passed. Partnering with Americans for Tax Reform, I’ve contributed to creating the Sustainable Budget Project, which monitors state government spending and evaluates the adoption of sustainable budgets across all states. This Project has a slightly different methodology and purpose than the one outlined above, as the focus is on spending at the end of a budget period instead of the one I’ve been using for appropriations at the start of the appropriations process. Together, these approaches can help states define the narrative about the need for spending restraint on the budget process’s front and back end. Given the excessive spending by governments and the incentive to continue doing so, there should be as many safeguards as possible. As Louisiana enters a new year with a new session and new governor this year, lawmakers have an extraordinary opportunity to prioritize sustainable budgeting by adopting what we’re calling a Responsible Louisiana Budget. The Pelican Institute released the first iteration of the RLB last year and the second one this year. This isn’t just about fiscal responsibility; it’s an effort that will help the people of Louisiana prosper. It will do so by helping Louisianans not be overburdened by unnecessary taxes for more money in their pockets. It’s Geaux Time in Louisiana, and that includes sustainable budgeting! Originally published at Pelican Institute. The report to achieve Louisiana’s 2024-2025 Responsible Budget presents solutions to rein in the extraordinary growth of the budget in order to give the state a competitive advantage, much like those used in other states, such as Texas and Florida, limiting the amount of funding appropriated at the beginning of each fiscal year. Over the past decade, state spending has increased an average of 5.9% per year. Using the recommended Responsible Budget growth limit outlined in this report, state spending would have increased by only 2.1% per year, which would allow the excess state revenue to be saved for tax relief for Louisiana families.  Originally published at James Madison Institute. Florida is an economic leader because it has produced pro-growth policies of lower government spending, taxes, and regulations for years. This strong institutional framework must continue. A new report, “Reducing the Burden of Sales Taxes in Florida,” authored by The James Madison Institute (JMI) Senior Vice President Sal Nuzzo and JMI Senior Fellow Vance Ginn, Ph.D., outlines recommendations for ways in which Florida lawmakers can reduce the government burden on citizens and businesses. “Florida continues to be the best place to start and grow a business. That requires us to continually examine ways to make it more attractive as states become more and more competitive. One way our policymakers and governor can do this is by addressing the sales tax allowance, which currently places us at a competitive disadvantage when looking at other states, especially within our region. By making this allowance more reflective of how much compliance truly costs, we can ensure that the principles of limited government and economic liberty advance.” — Sal Nuzzo, Senior Vice President, The James Madison Institute “Florida has been a key model for the country with a sound approach to conservative fiscal policy. This includes the commitment to a conservative state budget, no personal income tax, minimal corporate welfare, and sensible regulation. To retain the title of “Free State of Florida” and provide more opportunities that let people prosper, policymakers should continue championing policies that spend, tax, and regulate less so families and entrepreneurs can reach their full potential. Reducing the burden of collecting sales taxes on entrepreneurs by at least doubling the sales tax allowance and streamlining the collection process to reduce compliance costs will help achieve this goal while providing lower prices to families.” — Vance Ginn, Ph.D., Senior Fellow, The James Madison Institute Podcast: Is Texas Becoming Like California? TRUTH On State Spending, Property Taxes & More1/24/2024 This BONUS episode of the Let People Prosper show is with Bradley Swail, host of the Texas Talks podcast.

Today, we discuss: 1) Why "largest property tax relief in Texas history” became the second biggest due to excessive state spending and how the Lone Star State can eliminate the property tax for good; 2) The problem with a mandated minimum wage and reckless spending at the state and federal levels and; 3) Policies Texas leaders and lawmakers should adopt to strengthen the Texas model. Please like this video, subscribe to the channel, share it on social media, and provide a rating and review. Also, subscribe and see show notes for this episode on Substack (www.vanceginn.substack.com) and visit my website for economic insights (www.vanceginn.com).  Originally published at American Institute for Economic Research.

The Economist recently compared Joe Biden’s and Donald Trump’s economic records, concluding Biden wins so far. While the article raises valid points, it excludes key details that make the findings questionable. Ten months from now, there’s a high likelihood Biden and Trump could go head-to-head again for the presidency, especially after the results from the Iowa caucus. But voters should be informed about the effects of their policies on key issues like immigration, inflation, and wages. Starting with a divisive bang, let’s look at each leader’s track record concerning immigration. The Economist correctly noted that apprehensions along the southern border were much lower under Trump. They increased by the most in 12 years during the economic expansion of 2019, decreased early in the COVID-19 pandemic when people could be turned away for public health concerns, and rose again during the lockdowns. While some may see apprehensions rising between Trump and Biden as a loss for Biden, I see it as a loss for both. This metric is somewhat unreliable, given one person can be caught and counted multiple times, and those caught are a subset of total migrants. The truth is immigration is good for the economy, but government failures create unnecessarily complex barriers against legal immigration, contributing to the humanitarian crisis along the Mexico border today. Neither President has pushed for what’s needed (market-based immigration reforms) both lose. Inflation is another hot topic, especially for Biden. The Economist hands the win to Trump, as inflation was far lower during his presidency. But can we give him the credit? Remember, Trump pressured the Federal Reserve to reduce its interest rate target and expand its balance sheet, which was inflationary. His deficit spending skyrocketed during the lockdowns and was mostly monetized by the Federal Reserve, contributing to what was always going to be persistent inflation. Biden made this deficit spending and resulting inflation much worse. Add in the Fed’s many questionable decisions, such as doubling its assets, cutting and maintaining a zero interest rate target for too long, and focusing too much on woke nonsense, and we can see how this was always going to be persistent inflation. But even the Fed’s latest projections indicate it won’t hit its average inflation target of two percent until at least 2026. Likely, it will cut the current federal funds rate target range of 5.25 percent to 5.5 percent three times this year, keep a bloated balance sheet to finance massive budget deficits, and run record losses. If so, this inflation projection is too rosy. Some of Trump’s policies helped stabilize prices, including his tax and regulation reductions. But he still allowed egregious spending. Biden has doubled down on red ink that has contributed to the recent 40-year-high inflation rate. While inflation has been moderating recently under Biden, Trump gets the win. Of course, neither Presidents nor Congress control inflation, as that job is the Fed’s, but its fiscal policies influence it. When it comes to inflation-adjusted wages, The Economist grants a tie. Let’s consider real average weekly earnings that include hourly earnings and hours worked per week, adjusted for the chained consumer price index, which adjusts for the substitution bias and has been used for indexing federal tax brackets since the Tax Cuts and Jobs Act of 2017. Trump’s era witnessed a robust upward trajectory of real earnings, with considerable gains by lower-income earners, thereby reducing income inequality. We must acknowledge a real wage spike in 2020 during Trump’s lockdowns, marked by the loss of 22 million jobs and various challenges. To maintain a fair analysis, I disregard this spike. A year later, real wages demonstrated a decline under Biden. Extending the timeframe to two years later, real wages remain relatively flat to slightly increased. To provide a contextual understanding, when we consider the trend under Trump, excluding the 2020 spike, real wages for all private workers or production and nonsupervisory workers fall below those observed during Biden. It’s worth noting, however, that these wages have been higher since 2019, albeit nearly stagnant for all private workers. Given real earnings, I agree with The Economist that Trump and Biden are tied. While much more can be said for each President’s policies, continuing to add context when making assessments is crucial. I give Trump a nuanced “win” overall because his policies supported more flourishing during his first three years until the terrible mistake of the COVID lockdowns, with its huge, long-term costs. I should note that I made a strong case inside the White House for no shutdowns and less government spending but, alas, my efforts, and those by others, lost to Fauci, Birx, and Trump. Given the improved purchasing power during his presidency, Trump receives better poll ratings than Biden after three years of their presidencies. But this win doesn’t mean that Trump’s record is best regarding these issues, protectionism, and more. Let’s hope free-market capitalism, the best path to let people prosper, is on display this November, no matter who is on the ballot. Originally posted at South Carolina Policy Council. Thanks to a robust state economy, plentiful business opportunities, and a relatively low cost of living, South Carolina remains one of the fastest-growing states in the nation. To maintain this strong position and promote further growth, it is crucial for S.C. legislators to limit state spending and reduce the government’s burden on taxpayers. The S.C. Policy Council created the South Carolina Sustainable Budget (SCSB) to assist in this effort. The SCSB is a maximum limit on annual recurring general funds[1] appropriations based on the rate of state population growth plus inflation. First published in 2022 and again in early 2023, it has served as a data-driven resource to help rein in unsustainable spending and provide more opportunities for tax relief. Unfortunately, the state did not adhere to the SCSB limit of $11.20 billion for its fiscal year (FY) 2024 budget; instead, it appropriated $11.64 billion – a 12.56% increase above the FY23 base of $10.34 billion. To turn the tide of excessive budget growth and provide more room for tax relief, the Policy Council is issuing its third SCSB. Table 1 provides the results outlined in this report for the FY25 SCSB. Table 1. The FY25 South Carolina Sustainable Budget for Appropriations of Recurring General Funds  Based on population and inflation data in 2023, the recommended recurring general funds appropriations limit[2] for South Carolina’s FY25 budget is $12.27 billion. With inflation moderating somewhat since reaching a 40-year high in 2022, primarily because of the errant policies in D.C., the SCSB ceiling is higher than it would be under normal economic circumstances. For example, the average annual rate of population growth plus inflation since 2013 has been 3.78%. Accordingly, the S.C. Legislature should consider freezing spending at the current FY24 budget of $11.64 billion. This would help correct recent overspending in the state’s budget and help put the state on a more sustainable budget path. It would also leave more money available for needed tax relief. At a minimum, recurring general fund appropriations in the FY25 budget must remain below $12.27 billion. Overview A sustainable budget – sometimes called a conservative or responsible budget – is a model for state budgeting that sets a maximum limit on appropriations or spending based on the rate of population growth plus inflation. This metric serves as an indicator of what the average taxpayer can afford to pay for government provisions. It accounts for 1) More people in the state who could potentially pay taxes; 2) Wage growth that’s typically tied to inflation over time to pay taxes; and 3) Economies of scale, as not every new person or wage increase should be associated with new government spending. The SCSB does not make specific recommendations on how general funds should be appropriated in the budget. Instead, it gives legislators the flexibility to appropriate taxpayer dollars to government programs as determined by the General Assembly, while ensuring that spending growth remains in line with what people can afford. Such a voluntary spending limit is key to putting South Carolina in a position for further tax relief. In 2022, Gov. Henry McMaster and lawmakers enacted the first-ever state personal income tax cut, which immediately reduced the top rate from 7% to 6.5% and collapsed the lower bracket to 3%. It also scheduled additional yearly 0.1% cuts to the top rate until it reaches 6%, though general fund revenues must project at least 5% annual growth for the cuts to trigger. The problem with this approach is that it relies on continued revenue growth to deliver incremental tax relief. Following the SCSB would help to accelerate this process, freeing up revenue to buy down the top rate to 6% immediately and fueling other tax cuts. On the other hand, unsustainable spending could build pressure to reverse course and raise taxes, leaving South Carolinians with fewer opportunities to flourish. SC Appropriations vs. Sustainable Budget Figure 1 compares the previous twelve years[3] of South Carolina’s recurring general fund budget appropriations (FY13 to FY24) to those appropriations when limited each year to the rate of population growth plus inflation. Figure 1. South Carolina General Fund Appropriations v. SCSB 12-year GF appropriations: $98.5 billion (+91.1%) 12-year GF appropriations limited to population growth + inflation: $86.5 billion (+50.0%)  Notes. Budget amounts are based on data from South Carolina’s state budget publications, Fed FRED for state population growth and U.S. chained-CPI inflation, and authors’ calculations. Appropriations did not increase from FY20 to FY21 because the state operated on a continuing resolution in FY21.[4] Key takeaways (see Table 2):